The Cost of Delaying Retirement Savings

Compounding interest is a beautiful thing. Albert Einstein called it, “the greatest mathematical discovery of all time.” Compounding gives power to patient and disciplined investors to improve their lives, and their families, for the better. The basic formula for compounding gains has three main variables: dollars invested, rate of return, and time. While the vast majority of financial articles focus on getting the highest rate of return, it is just one of the three variables. Let’s look into the other two variables that we have much better control over.

Saving dollars rather than using them to spend or pay down debt takes discipline and hope for the future. While sometimes we make the savings decision after receiving a bonus, sale of a property or business, or inheritance, most of the time the decision to save is made on a regular ongoing basis. For most people the easiest way to save is through an automatic deduction from wages or a bank account, just like a bill. In any case, your rate of return won’t matter much if you don’t save and invest much money.

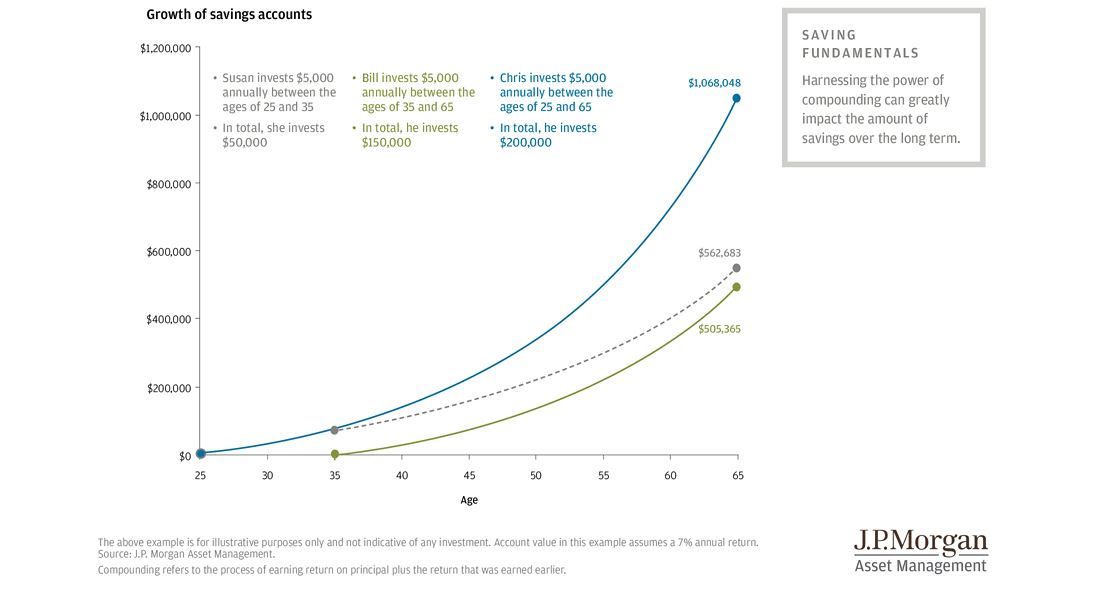

The third input into the compounding equation is time, which is most certainly not to be overlooked. The chart above shows a the hypothetical growth of three investors who save the same amount each year and earn the same rate of return, but save during different years. The comparison that stands out the most is between Bill and Chris. Bill saves $5,000 per year for 30 years from age 35 to 65, or $150,000 in all. Chris saves the same $5,000 per year, but starts ten years sooner at age 25, investing $200,000 in total. In the end, Chris has saved 33% more, but ends up with more than double what Bill’s account has grown to.

In a world fixated on rate of return as the key variable to investing success, let’s try to keep it in perspective with the other two very important variables of savings and time.